Family succession and tax planning: Navigating intergenerational business transfers

By Danielle Walsh

It is hard to transition a business to the next generation. Especially when you’re leaving significant tax dollars on the table. The potential loss could substantially affect your ability to retire comfortably.

Bill C-208, which became law on June 29, 2021, represented a significant milestone in Canadian tax legislation, particularly for families considering intergenerational business transfers (IBTs). This private member’s bill aims to provide certain family businesses with the opportunity to access the lifetime capital gains deduction on intergenerational transfers, aligning their tax treatment with businesses sold to third parties.

Before Bill C-208, selling a business to a family member meant a tax result that was less favourable than selling to a third party. In this article, we will delve into the key aspects of the Bill C-208 changes, and the additional changes proposed in the 2023 federal budget, exploring the implications for family businesses.

Family succession planning vs. tax planning

While tax planning is important and can play a key role in your succession plan, you should not allow it to guide the succession process. These two aspects need to work together to maximize family harmony and ensure a sound tax plan. It is important for family decisions to minimize the possibility of creating further conflict, resentment, and confusion about the future.

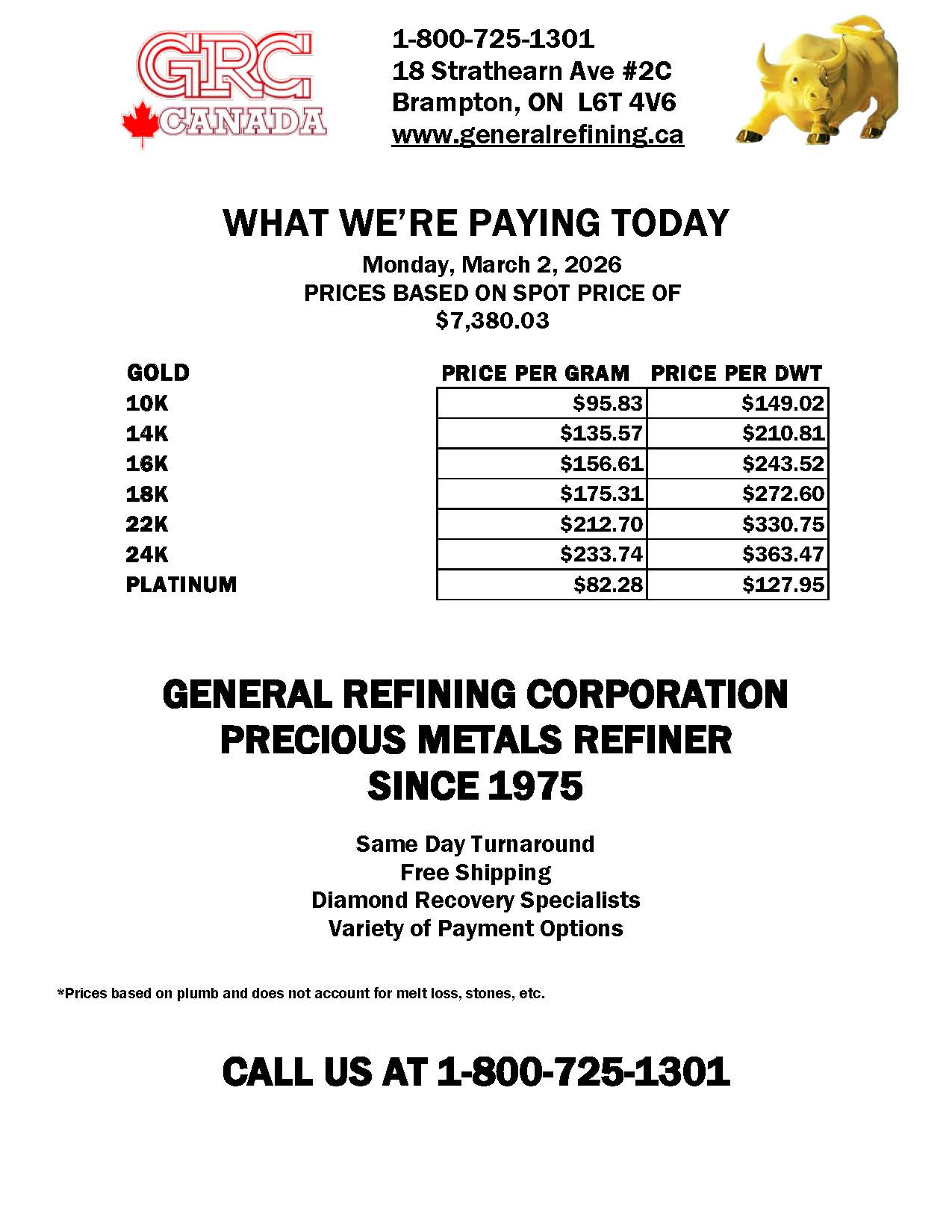

For instance, I recently spoke with two parents who own a jewellery store. In order to access the tax treatment on IBTs following the Bill C-208 changes, and to do so equally between their two children, they gave each child five per cent of the family business. The eldest son, Michael, has worked in the business full-time over the last five years. In his mind, he has been working towards management and potentially ownership. His younger brother, Justin, has never worked in the jewellery store, nor has he ever shown an interest in it.

Soon after their decision, the parents noticed that the relationship between their children started to degrade, but they weren’t sure why. Michael was upset that his younger brother, who had not worked in the business and did not plan to work in the business, got the same ownership percentage. Michael started to wonder if, down the road when his parents decided to retire, he would have to continue to split ownership with Justin. He asked his parents, but they did not have an answer, which frustrated Michael further and led him to take a break from working in the business.

His parents couldn’t believe the impact their tax planning decision had on family dynamics. Mom and dad finally realized that, while tax planning was important, it created questions, concerns, and unknowns in the family they hadn’t been able to answer, but should have considered beforehand. Families need to take a more integrative approach to succession. Your tax, estate, and succession advisors should be working together to ensure a plan that works on all fronts.

Tax planning is important, but it should not guide your long-term decision-making with respect to the succession plan of your family business. Not communicating why, who, and how shares will be distributed now and in the future can be a recipe for disaster. Even providing a small percentage of ownership to the next generation without a clear plan can result in the opening of a “can of worms.”

Families need to be able to answer the following questions to minimize conflict amongst the next generation:

- Do all children need to own together in the future? Or does one child need to buy their siblings out?

- The children are not compatible, now what?

- What about children who have never worked in the business? Moving forward, will they get more ownership than those who have?

- Is the business an inheritance?

- If one child contributes more to the business, why would they continue to do so if their siblings—who work outside the family business—obtain equal ownership? What is the value of their contributions?

Benefits of current IBT rules

Ideally, you build a succession plan that answers the above questions and then make it as tax efficient as possible. Of course, if there is an easy way to tweak the plan to be tax efficient, we will! That is why it is important for business owners like yourselves to understand the parameters of the IBT rules and how they may or may not apply to you.

One of the notable benefits of the IBT rules is that it grants access to the lifetime capital gains deduction for qualifying intergenerational transfers. This deduction, which represents approximately $240,000 to $278,000 of tax savings per taxpayer (based on 2024 rates), provides a considerable financial benefit for those involved in the transfer of qualified small business corporation shares or shares of a family farm or fishing corporation.

Capital gains deduction

Taxpayers should always consider the availability of their lifetime capital gains deduction (CGD), which can be utilized on the sale of qualified farm or fishing property (QFFP) or qualified small business corporation shares (QSBC). The specific requirements to meet the definition are beyond the scope of this article, but you should not assume that your shares qualify—there are many traps that could throw you offside of the tests.

At a high level, access to the CGD depends on whether the corporation is a QSBC or QFFP at the time of the disposition. The qualification is dependent on both a test of the assets of the company and the length of share ownership. The company is required to be a Canadian-controlled private corporation (CCPC) and simply put, you or someone related to you must have owned the shares for at least 24 months (subject to a few exceptions) prior to the sale. In the 24 months preceding the sale, more than 50 per cent of the company’s assets must have been used in an active business operating in Canada—with this threshold increasing to 90 per cent at the moment of sale. These rules, simplified for illustration in this article, become more complicated with a multi-company structure or a parent/subsidiary structure.

Proposed amendments in the 2023 federal budget

The 2023 federal budget introduced amendments to the rules established by Bill C-208 to safeguard against potential abuse. The amendments aim to ensure the legislation applies exclusively to authentic intergenerational business transfers. Among the amendments, the definition of “child” for IBT purposes is expanded to include nieces, nephews, grandnieces, and grandnephews in addition to children, stepchildren, and children-in-law.

Further, the 2023 federal budget imposes additional conditions on intergenerational share transfers to be eligible for the rules introduced through Bill C-208. Taxpayers must now rely on one of two transfer options, where all criteria are met.

Immediate business transfer (three-year test)

- Parents transfer both legal and factual control over three years.

- Parents immediately transfer a majority of the voting shares and common shares, with the balance to be transferred within 36 months.

- Parents transfer management of the business to their child within a reasonable time based on the particular circumstances (with a 36-month safe harbour).

- Child(ren) retains legal (not factual) control for at least 36 months following the share transfer.

- At least one child remains actively involved in the business for 36 months following the share transfer.

Gradual business transfer (five to 10-year test)

- Parents immediately transfer only legal control

- Parents immediately transfer a majority of the voting shares and common shares, with the balance to be transferred within 36 months. Further, within 10 years of the initial sale, the parents must reduce the value of their economic interest (amounts owed and equity) in the business to either:

- 50 per cent of the value of their interest in the family farm or fishing corporation at the initial sale time, or

- 30 per cent of the value of their interest in the qualified small business corporation at the initial sale time.

- Parents transfer management of the business to their child within a reasonable timeframe based on the particular circumstances (with a 36-month safe harbour).

- Child(ren) retains legal (not factual) control for at least 60 months following the share transfer.

- At least one child remains actively involved in the business for at least 60 months following the share transfer.

Conclusion

The changes to IBTs introduced through Bill C-208 represent a significant development in Canadian tax law, offering family businesses an opportunity to use their capital gains deduction during intergenerational transfers. The potential benefits, including access to the lifetime capital gains deduction and flexibility in family shareholder arrangements, make it a valuable tool for succession planning.

However, to minimize conflict and maintain family harmony, it is wise to implement IBTs once you have a family business succession plan that the entire family is aware of and understands. Doing so allows you to maximize the family harmony and ensure a tax efficient transition!

Danielle Walsh is a chartered professional accountant (CPA), chartered accountant (CA), and holds certificates in family business advising and family wealth advising from the Family Firm Institute (FFI). Walsh developed her philosophy and desire to help family businesses from her father, Grant Walsh, who has worked as a family business practitioner for more than 25 years. She and her father published a book titled, A Practical Guide to Family Business Succession Planning: The Advice You Won’t Get from Accountants and Lawyers. She recently joined MNP as a partner, focusing on succession. She can be reached at danielle.walsh@mnp.ca.

Sign up for our newsletter

Get all the latest news and features from Jewellery Business. Submit your email below to get our twice-monthly newsletter.

Related Products

Read the Latest Issue